VA Loan: Marine Veteran Purchases First Home Without Down Payment

Educational Case Study Disclosure

This case study is hypothetical and for educational purposes only. Scenarios, borrower profiles, loan terms, interest rates, and outcomes are illustrative examples and do not represent current offers or guaranteed terms.

For specific details including down payment requirements, closing cost estimates, interest rate details, closing cost breakdowns, payment calculations, cash-to-close estimates, or an official Loan Estimate, it is highly recommended you schedule a meeting with one of our licensed mortgage advisors.

Learn more:

- VA loan Reg Z advertising requirements (§1026.24) – CFPB official regulation

- VA loan Reg Z full text and compliance – Electronic Code of Federal Regulations

- Official VA loan advertising interpretations (§1026.24) – CFPB interpretations

- VA loan MAP Rule (Reg N) mortgage advertising – Mortgage advertising rules

- NMLS Consumer Access – Verify VA loan lender licensure

Actual loan terms vary by credit profile, property, occupancy, location, market conditions, and lender guidelines. For current options tailored to you, schedule a consultation or apply online.

Ready to explore your options? Schedule a call with a loan advisor.

Discover How a VA Loan Made Homeownership Accessible Without Savings

Sergeant Carlos M., a 29-year-old Marine Corps infantry veteran based in San Diego, earned a respectable mid-five-figure income working as a logistics coordinator for a defense contractor after completing six years of active duty service. After years of moving between military bases and deployments to multiple locations, Carlos was ready to put down roots and purchase his first home—a place to build equity instead of paying rent and to start creating generational wealth for his future family.

Despite earning stable income and maintaining excellent credit, Carlos faced a significant obstacle: he had minimal savings for a down payment. Between student loans from his post-service education, a modest car payment, and the high cost of living in San Diego, Carlos hadn’t been able to accumulate substantial savings. He watched friends and colleagues buying homes with conventional financing, but their down payment requirements seemed impossibly out of reach.

Facing similar challenges? Schedule a call to explore your options.

The Challenge: Why Down Payment Requirements Blocked Homeownership

How Do Traditional Home Loans Work for First-Time Buyers?

Carlos initially researched conventional financing and FHA loans through online lenders and local banks. Every option required substantial down payments—conventional loans wanted significant cash down for competitive rates, while FHA required smaller down payments but added expensive mortgage insurance that would increase his monthly payment substantially and persist for years.

Why Was Carlos Unable to Save for Down Payment?

“I was making decent money and had excellent credit, but I was also paying off student loans and dealing with San Diego’s insane cost of living,” Carlos explained. “My rent was eating up a huge portion of my income, and every time I started to build savings, something would come up—car repairs, medical bills, helping family. I felt trapped in a cycle where I was paying someone else’s mortgage through rent but couldn’t save enough to get into my own home.”

Carlos faced the classic catch-22 of renting: His monthly rent was comparable to what a mortgage payment would be, but he couldn’t save for a down payment because rent consumed so much of his income. Meanwhile, home prices in San Diego kept rising, making the down payment target a moving goalpost.

What Obstacles Did Carlos Face with Conventional and FHA Financing?

Beyond the down payment challenge, Carlos discovered other barriers to conventional homeownership:

- Conventional loans: Required substantial down payment for decent rates, plus private mortgage insurance if putting down less than a certain threshold, which would significantly increase monthly payments

- FHA loans: Smaller down payment option but required expensive mortgage insurance premiums—both upfront and monthly—that would persist throughout the life of the loan unless he refinanced

- Gift fund restrictions: Carlos’s parents wanted to help, but lenders had strict rules about gift funds and required extensive documentation proving the money was a gift rather than a loan

- Closing cost barriers: Even with down payment assistance programs, closing costs presented another substantial hurdle

How Did Down Payment Requirements Threaten Carlos’s Goals?

With each passing month of rent payments, Carlos calculated how much equity he could have been building if he owned his home. The frustration was compounded by the fact that he’d served his country honorably for six years, survived multiple combat deployments, and was now being told he couldn’t access the American dream of homeownership because he didn’t have cash savings—despite earning good income and having excellent credit.

“I felt like I’d done everything right—served my country, got education after service, landed a good job, paid my bills on time, maintained excellent credit—but none of that mattered because I didn’t have a pile of cash sitting in the bank,” Carlos said. “Meanwhile, I was paying rent every month that was building someone else’s wealth instead of my own.”

Experiencing similar rejection? Schedule a call to discuss alternative qualification methods.

The Discovery: How Carlos Found VA Loan Programs

How Did Carlos Discover VA Loan Benefits?

During a conversation with a fellow Marine veteran at a defense contractor networking event, Carlos mentioned his frustration with down payment requirements. His colleague immediately stopped him: “Wait—have you looked into your VA loan benefit? I bought my house with zero down payment using my VA loan. No down payment, no PMI, competitive rates. It’s one of the best benefits we earned through our service.”

Carlos was stunned. He’d heard vague references to VA loans during his transition briefing when leaving active duty, but no one had explained the zero-down benefit clearly or emphasized how powerful it was for first-time homebuyers without substantial savings.

What Makes VA Loans Different from Conventional Financing?

That evening, Carlos researched VA loan programs extensively and scheduled a consultation with a VA loan specialist at Stairway Mortgage. During the call, the specialist explained the key benefits that Carlos had earned through his military service:

- Zero down payment required: Eligible veterans can purchase homes with no down payment whatsoever—the loan covers the full purchase price

- No private mortgage insurance (PMI): Unlike conventional loans or FHA loans, VA loans don’t require monthly mortgage insurance, significantly reducing monthly payments

- Competitive interest rates: VA loans typically offer rates as good or better than conventional financing

- Flexible credit requirements: VA lenders can work with veterans who have less-than-perfect credit

- Limited closing costs: VA regulations cap fees lenders can charge, and sellers can pay some closing costs

- No prepayment penalty: Veterans can pay off VA loans early without penalty

- Assumable loans: Future buyers can assume the VA loan, potentially making the home more attractive when Carlos eventually sells

Why Are VA Loans Better for Military Veterans Without Savings?

“That consultation changed everything,” Carlos said. “For the first time, someone explained that my military service had earned me a benefit specifically designed to overcome the down payment barrier. This wasn’t charity or assistance—it was a benefit I’d earned through six years of service and multiple deployments. The VA loan program recognized that veterans shouldn’t be blocked from homeownership just because they don’t have cash savings, especially when they have stable income and good credit.”

The VA loan specialist explained that Congress created this benefit specifically to help veterans achieve homeownership—recognizing that military service often leaves veterans with limited savings due to frequent moves, deployments, and lower military pay compared to civilian careers.

The Solution: VA Loan Approval Process

What Documentation Was Required for VA Loan Approval?

Carlos worked with his VA loan advisor to assemble the required documentation. While he didn’t need a down payment, he still needed to qualify based on income, credit, and debt-to-income ratio, just like any mortgage.

Documentation provided:

- Certificate of Eligibility (COE) obtained from VA confirming loan benefit

- DD-214 (Certificate of Release or Discharge from Active Duty)

- Standard income verification (pay stubs, W-2s showing stable contractor income)

- Credit reports showing excellent credit score and responsible payment history

- Employment verification from defense contractor

- Minimal reserves required (far less than conventional financing)

- Bank statements showing ability to cover modest closing costs

How Long Does VA Loan Approval Take?

The approval process:

- Certificate of Eligibility obtained – VA confirmed loan eligibility within days

- Pre-qualification – Verified income and credit qualified Carlos for target purchase price

- Home search – Carlos worked with realtor to find suitable home within budget

- Purchase contract – Made offer on 3BR/2BA home in Chula Vista

- Loan application submitted – Completed formal application with VA lender

- Underwriting approval – VA loan lender approved based on income and credit

- VA appraisal – Property appraised at purchase price, confirming value

- Clear to close – Final approval issued

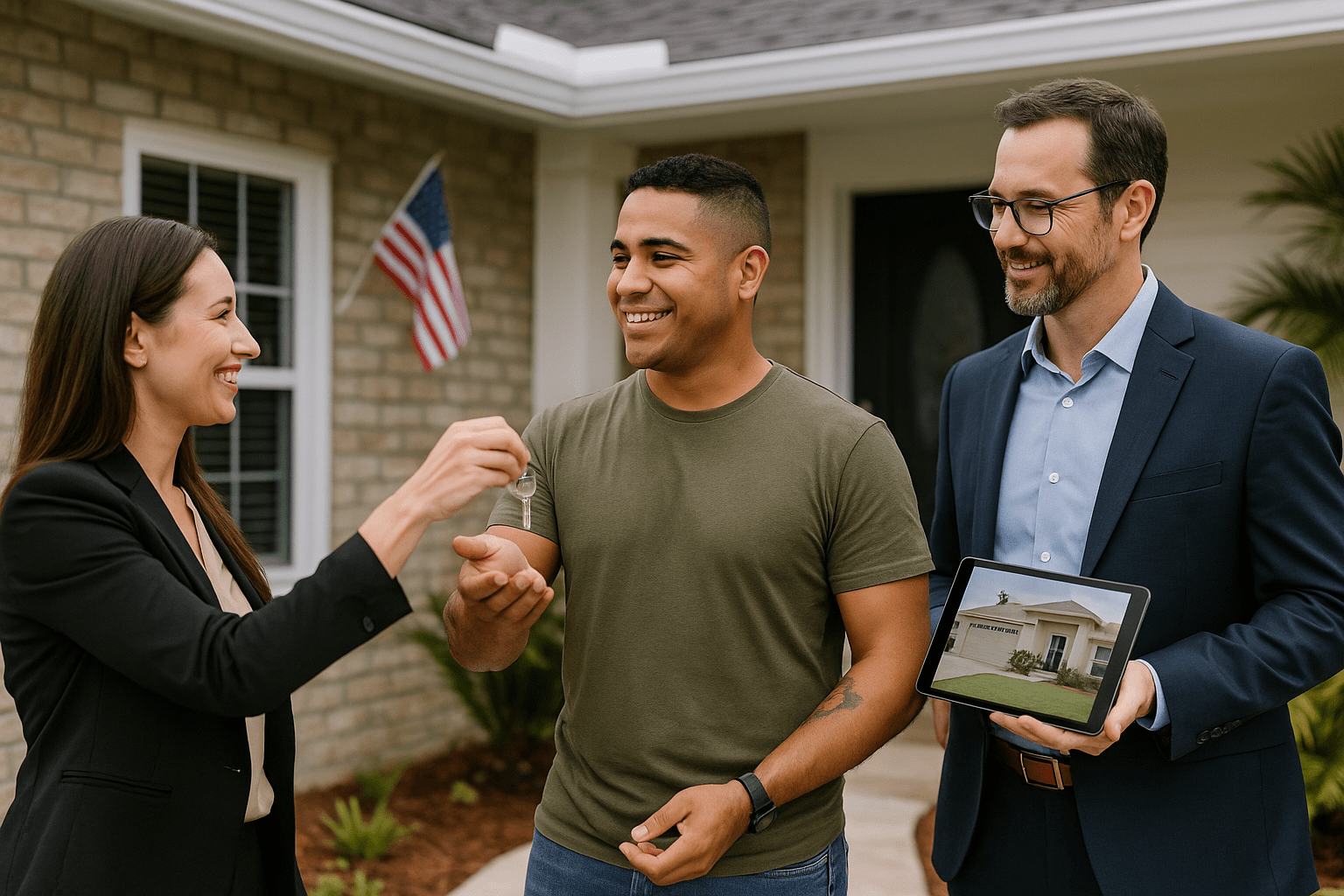

- Closing – Signed documents and received keys with zero down payment

What Steps Were Involved in the VA Loan Process?

The VA loan lender walked Carlos through each step, explaining that while he didn’t need a down payment, he would need to pay a VA funding fee (which was added to his loan balance rather than paid out-of-pocket) and standard closing costs. However, Carlos’s seller agreed to contribute toward closing costs, and Carlos only needed to bring minimal funds to closing—far less than any conventional or FHA option would have required.

“The process was straightforward,” Carlos explained. “My VA loan advisor explained everything clearly, responded quickly to questions, and kept the process moving. Within forty-five days from accepting my offer to closing day, I went from renter to homeowner without depleting my modest savings for a down payment. The monthly payment was comparable to my rent—except now I’m building equity instead of paying a landlord.”

Ready to purchase? Submit a purchase inquiry to discuss your scenario.

The Results: Carlos Closes on First Home Without Down Payment

What Results Did Carlos Achieve with VA Loan?

Carlos closed on his first home approximately forty-five days after his offer was accepted. The three-bedroom, two-bathroom home in Chula Vista—a San Diego suburb with good schools and access to his workplace—met all his criteria. Most importantly, he purchased it without depleting his savings for a down payment.

Final loan outcome:

- Approved loan amount covered full purchase price with zero down payment

- Competitive interest rate comparable to conventional financing

- No monthly mortgage insurance—substantially lower payment than FHA alternative

- Standard long-term fixed-rate mortgage structure

- Timeline: Offer acceptance to closing in approximately 45 days

- Property: 3BR/2BA single-family home, Chula Vista, CA

- Monthly payment comparable to previous rent—building equity instead of paying landlord

How Did VA Loan Compare to Conventional and FHA Financing?

Conventional/FHA vs. VA loan comparison:

- Conventional requirement: Substantial down payment required (or expensive PMI)

- FHA requirement: Smaller down payment but expensive mortgage insurance throughout loan

- VA loan benefit: Zero down payment, no mortgage insurance

- Monthly payment difference: Substantially lower with VA loan due to no PMI/MIP

- Out-of-pocket at closing: Minimal with VA loan vs. substantial with conventional/FHA

- Homeownership timeline: IMMEDIATE vs. years of saving ✓

What Would Have Happened Without VA Loan?

“Without my VA loan benefit, I’d probably still be renting and trying to save for a down payment—a goal that kept getting further away as home prices rose,” Carlos admitted. “Instead, I’m a homeowner building equity every month. The amount I would have paid in rent over the next few years alone would have been substantial—now that money is going toward building my own wealth instead of someone else’s.”

How Does Carlos Plan to Build Long-Term Wealth?

Carlos views this home as the foundation of his wealth-building strategy. “This isn’t just about having a place to live—it’s about building equity, establishing credit, and creating a foundation for my financial future,” Carlos explained. “In five to ten years, I’ll have built substantial equity in this home. At that point, I could either sell and upgrade to a larger home, or I could keep this property as a rental when I’m ready to buy my next home.”

Carlos plans to leverage his growing equity strategically. “When I’m ready for my next property—whether that’s upgrading my primary residence or buying a rental property—I’ll explore using a HELOC or Home Equity Loan on this property to access the equity I’ve built without refinancing and losing my current favorable rate. That’s how you build wealth—using the equity from property #1 to acquire property #2, then repeating the process.”

Ready to get started? Get approved or schedule a call to discuss your situation.

Exploring Other VA Loan Options?

While Carlos used a VA loan to purchase his first home, VA financing works for multiple scenarios:

- Already own and want to lower payment? See how a Navy veteran reduced monthly costs with VA IRRRL streamline refinance

- Need cash for improvements? See how an Air Force veteran accessed equity with VA loan cash-out refinance

- Want to build custom home? See how a Navy veteran built dream home with VA construction loan

- View all case studies to find success stories matching your situation

Key Takeaways for Military Veterans Pursuing First Homes

- VA loans eliminate down payment barriers for eligible veterans—service members and veterans with appropriate length of service can purchase homes with zero down payment, removing the primary obstacle to homeownership for those without substantial savings (VA loan eligibility requirements)

- No monthly mortgage insurance significantly reduces payments—unlike conventional loans requiring PMI or FHA loans requiring MIP, VA loans have no monthly mortgage insurance, resulting in substantially lower monthly payments for the same purchase price (VA loan benefits overview)

- Competitive rates and flexible credit standards—VA loans typically offer rates comparable to or better than conventional financing, with more flexible credit requirements that help veterans with less-than-perfect credit qualify (HUD VA lender handbook)

- VA funding fee can be rolled into loan amount—while VA loans require a funding fee, it can be financed into the loan balance rather than paid out-of-pocket, preserving veteran’s savings

- Think beyond the first home toward wealth-building—homeownership is the foundation of wealth creation, allowing veterans to build equity rather than paying rent, establish strong credit, and create a platform for future investment properties or upgrading to larger homes as families and finances grow

Have questions about qualifying with VA loan benefits? Schedule a call with a loan advisor today.

Alternative Loan Programs for Military Veterans and First-Time Buyers

If a VA loan isn’t the perfect fit, consider these alternatives:

- FHA Loan – Low down payment option for non-veterans

- Conventional Loan – Standard financing with various down payment options

- VA Construction Loan – Build custom homes with VA benefits

- USDA Loan – Zero-down financing for rural areas

- First-Time Home Buyer Programs – State and local assistance programs

Explore all loan programs to find your best option.

Helpful VA Loan Resources

Learn more about this loan program:

- Complete VA Loan Guide – Detailed requirements, rates, and qualification guidelines

- VA Loan Calculator – Estimate your qualification and payments

Similar success stories:

- Navy veteran reduced monthly costs with VA IRRRL streamline refinance – Rate reduction success story

- Air Force veteran accessed equity with VA loan cash-out refinance – Using equity for improvements

- View all case studies – Browse by your journey stage

External authoritative resources:

- VA loan eligibility requirements – Official VA guidance

- VA home loan benefits overview – Complete benefit details

- HUD VA lender handbook – Industry standards

Ready to get started?

- Apply online – Start your application today

- Schedule a consultation – Discuss your specific situation

- Take the discovery quiz – Clarify your goals

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and financial advisors in your area.

Need a Pre-Approval Letter—Fast?

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

- Only 2 minutes to complete

- Quick turnaround on pre-approval

- No credit score impact

Got a Few Questions First?

Not Sure About Your Next Step?

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

- Takes just 5 minutes

- Tailored results based on your answers

- No credit check required

Related Posts

Subscribe to our newsletter

Get the latest insights and mortgage case studies in your inbox.